Fed officials are posturing as though the first rate hike will occur in December.

They view a rate hike as affirmation that monetary policy measures have been successful.

The problem is that the Fed is still far from achieving its mandate.

The Fed will find an excuse to not raise rates in December.

Six Federal Reserve officials spoke yesterday, collectively leaning towards a December interest-rate hike. New York Fed President William Dudley commented that the risks of moving too quickly to raise interest rates were now “nearly balanced” with the risks of moving too slowly, which is a departure from his dovish stance on rates. He also warned that the unemployment rate of 5% could fall further, stoking inflation, and that the seven-year period of zero-interest-rate-policy “may be distorting financial markets.” May be distorting financial markets?

The stock market was none too happy to hear that the free-money parade may be coming to an end. The futures market has now priced in a 70% probability that the Fed will raise rates by year-end. The S&P 500 (NYSEARCA:SPY) slid 1.4%, while the Russell 2000 (NYSEARCA:IWM) plunged 1.9%. As though pandering to an unruly child, Chicago Fed President Charles Evans assured us that rate hikes would be gradual and probably reach less than 1% by the end of next year. Financial markets were not reassured.

I sense a Fed that is panicking behind closed doors. It is grasping for green shoots that it hopes will signify that its seven-year long monetary experiment has been a success. The problem is that those green shoots are really dead weeds. The Fed’s employment mandate may have been achieved with the headline unemployment rate of 5%, but that masks a labor force that is far weaker than the number suggests. If it were a sign of economic strength, we would already be seeing rising rates of real income and consumer spending. These have yet to materialize. We would also see a healthy inflation of 2% or more instead of the disinflation that has strangled our economy. Still, the Fed is hoping that it has enough good scores on the economic front by year-end to receive a passing grade for its policies, exclaim “mission accomplished,” and begin the process of normalization. I do not see this happening. I think there is no chance of a December rate hike.

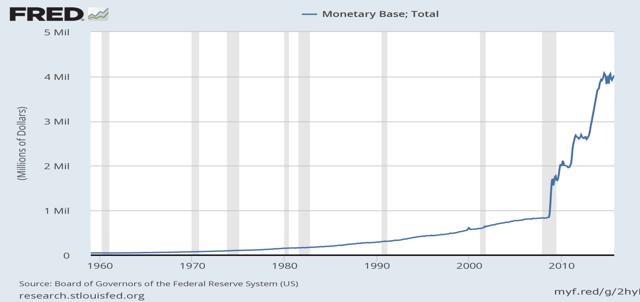

The Fed has expanded the monetary base a staggering 400% since the financial crisis by buying Treasuries and mortgage-backed securities from the banks, with the intent that the banks would lend the money to consumers.

(click to enlarge)

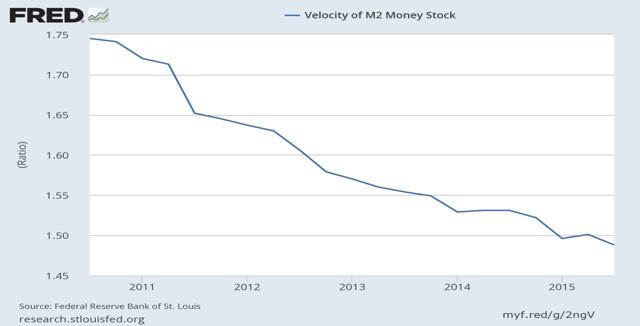

Instead, the money was predominately invested back into financial markets. The debt-laden consumers that needed credit could not obtain it, while those who could didn’t have a demand for it. As a result, the velocity of money has continued to decline, meaning that the money that is in the economy is circulating at a slower rate. If the economy were strengthening, the velocity of money would be rising.

(click to enlarge)

I do not understand how the Fed can believe that it is remotely close to achieving its inflation mandate of stable prices, or a rate of inflation that approaches 2%. The inflation rate peaked at 4% in 2011 before declining to what is near zero presently, but this is largely due to the fall in energy prices.

(click to enlarge)

If we exclude food and energy prices, the core rate of inflation is approaching 2% as it did in 2014, but is it sustainable?

(click to enlarge)

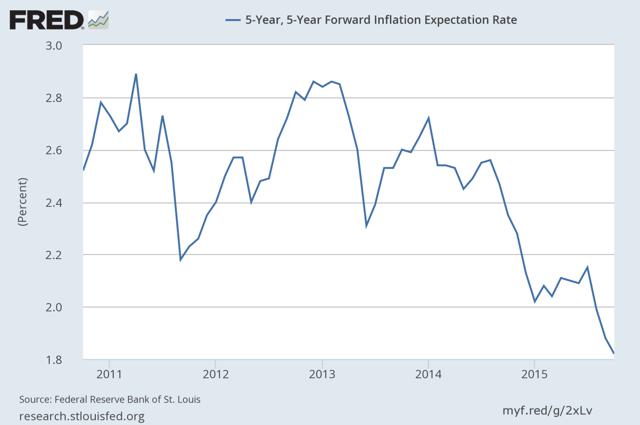

Considering the fact that these are lagging indicators, telling us more about the past than what may happen in the future, the Fed should be, and I believe is, focusing on inflation expectations. As can be seen below, expectations have been falling steadily over the past two years.

(click to enlarge)

Lastly, there is what I view to be the most valuable leading economic indicator of them all for our consumer-based economy – the rate of growth in consumer spending. The steady downtrend in sales, as can be seen below, is not indicative of an economy that is strengthening, as several Fed policy makers suggest.

(click to enlarge)

The Fed will find another excuse to keep rates at zero through the end of the year. It will be the IMF, or China, or retail sales, or market instability and volatility, or the weather. The excuse doesn’t matter. The reason is that it has not achieved its mandate, and it greatly fears the repercussion for the economy of deflating the one thing it has managed to inflate – financial assets.

No comments:

Post a Comment